Search

A Quarterly Post-World War II Real GDP Series for New Zealand

Published: 2007

Authors: Viv Hall, John McDermott

There are two essential features of macroeconomic data: growth and business cycles. To understand both phenomena, you need a long historical record.

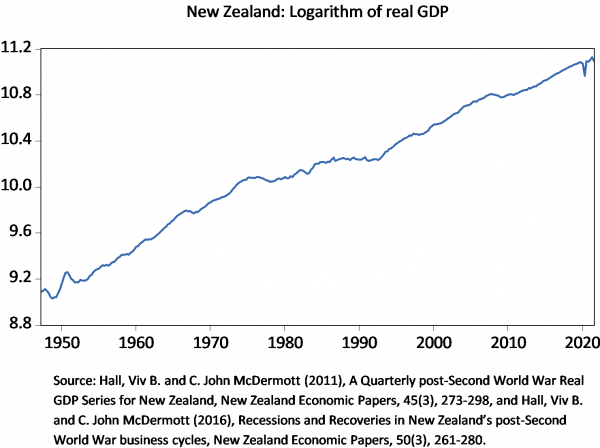

Unfortunately, official New Zealand data on quarterly real Gross Domestic Product (GDP) only goes back to 1987, limiting our ability to understand the nature of growth or the frequency of recessions.

Viv Hall and John McDermott provide estimates of quarterly GDP back to 1947, providing 75 years worth of economic history we can use to deepen our understanding of the New Zealand economy. Hall and McDermott used a range of econometric methods to estimate a quarterly GDP series using annual GDP data and quarterly economic indicators. The work originated as a Motu Working Paper (see link to the working paper version on this page) and was subsequently updated in a couple of peer reviewed articles (see Hall and McDermott (2011 and 2016).

They develop a seasonally adjusted series for 1947q2 to 2006q2, by linking quarterly observations from two recent official series to temporally disaggregated observations for an earlier time period. Annual real GDP series are disaggregated, using the information from two quarterly diffusion indexes, developed by Haywood and Campbell (1976).

Three econometric models are used: the Chow and Lin (1971) model that disaggregates the level of GDP, and the Fernández (1981) and Litterman (1983) models that disaggregate changes in GDP. Statistical properties of the series are evaluated and movements in the new series are benchmarked against qualitative research findings from New Zealand's post-WWII economic history.

Our preferred quarterly series is based on results generated from the Chow-Lin model.

See here for an updated version of data. See the below graph for a summary of the data.

You can also access the data directly:

In Python use the following code:

import pandas as pd

import requests

url = "https://www.motu.nz/assets/Documents/our-research/Macroeconomics/Real_GDPseries_1947q2-2022q3_at-15-Dec-2022.xlsx"

pullDf = requests.get(url).content

df = pd.read_excel(pullDf)

In EViews use the following code (with R interface):

wfcreate(wf=Hall_McDermott_data, page=quarterly) q 1947q2 2022q4

xopen(r)

xon

library(openxlsx)

library(fpp)

urlgdp <- "https://www.motu.nz/assets/Documents/our-research/Macroeconomics/Real_GDPseries_1947q2-2022q3_at-15-Dec-2022.xlsx"

realgdp <- read.xlsx(urlgdp)

ts_realgdp <- ts(realgdp$X2[9:nrow(realgdp)], start=c(1947, 2), frequency=4)

xoff

xget(type=series) ts_realgdp @smpl 1947q2 2022q4

xclose(r)

In R use the following code:

library(openxlsx)

library(fpp)

urlgdp <- "https://www.motu.nz/assets/Documents/our-research/Macroeconomics/Real_GDPseries_1947q2-2022q3_at-15-Dec-2022.xlsx"

realgdp <- read.xlsx(urlgdp)

ts_realgdp <- ts(realgdp$X2[9:nrow(realgdp)], start=c(1947, 2), frequency=4)

Level 1, 97 Cuba Street, PO Box 24390

Wellington 6142, New Zealand

Phone: 64 4 939 4250